Inflation and the Fed

Last week, the Federal Reserve announced no change to interest rates and threw water on any hopes for a rate cut at its next meeting in May.

This more-tempered outlook for interest rates stands in contrast to market expectations in late 2023. In November of last year, after nearly two years of sharply rising interest rates, Fed officials first spoke of rate cuts. In celebration, markets rallied in what became known as the “pivot party.” In fact, from its low in October, the S&P 500 has risen over 25%, a remarkable rally in a short period of time.

Bond markets too celebrated. The yield on the ten-year Treasury bond declined by nearly one full percentage point. By the end of December, futures markets were predicting that the Fed would cut rates a remarkable seven times this year.

Those frothy rate cut expectations stand in stark contrast to current expectations of just three rate cuts in 2024 and a more sober Fed outlook. So why the newfound caution?

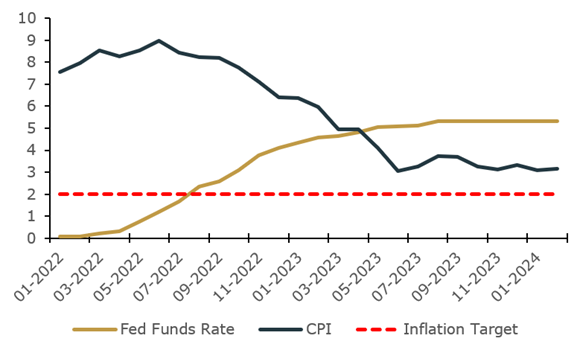

The short answer is that the economy continues to run hotter than Fed officials would like.

CPI vs Federal Funds Rate (%)

Source: Kestra Investment Management with data from FRED

In Fed Chair Jerome Powell’s words, inflation in January and February remains too high and other data suggested that the labor market was hotter than expected. Those indicators and other data have pushed up estimates for economic growth this year from a below-average 1.4% to a more average rate of 2.1%.

This trend suggests that remains a threat and that the economy is less in need of a boost from lower interest rates. As Powell highlighted, the Fed faces a much-discussed two-sided risk: ease too much too soon, and inflation comes back. Ease too late, and risk doing unnecessary harm to jobs.

For now, the main impact has been to push rate cuts to later in the year and slow the pace of those cuts. But one other factor will further complicate the Fed’s job: November’s presidential election. Typically the central bank is reluctant to change policy close to an election for fear of influencing, or even to be seen as influencing, results. That timing would suggest that Federal Reserve officials either begin rate cuts sooner, to get them out of the way, or simply wait until after the election.

Over the next couple of months, data on inflation and the labor market will help Chairman Jerome Powell and his colleagues perform their delicate balancing act between supporting economic growth and containing inflationary pressures. For now, though, policymakers remain on pause.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, and Bluespring Wealth Partners, LLC. The material is for informational purposes only. It represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. It is not guaranteed by any entity for accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was created to provide accurate and reliable information on the subjects covered but should not be regarded as a complete analysis of these subjects. It is not intended to provide specific legal, tax or other professional advice. The services of an appropriate professional should be sought regarding your individual situation. Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, and Bluespring Wealth Partners, LLC do not offer tax or legal advice.